The story we tell about the world’s most powerful companies is almost always the wrong one.

We tell it as a biography. A founder with a vision. A garage, a dorm room, a chance meeting. Early struggles, near-death experiences, a breakthrough moment. Then success, exponential, inevitable in retrospect. The mythology is compelling because it’s human. It centers character and will and genius in a way that makes the outcome feel earned through personal virtue.

It also systematically obscures the structural realities that actually explain corporate power.

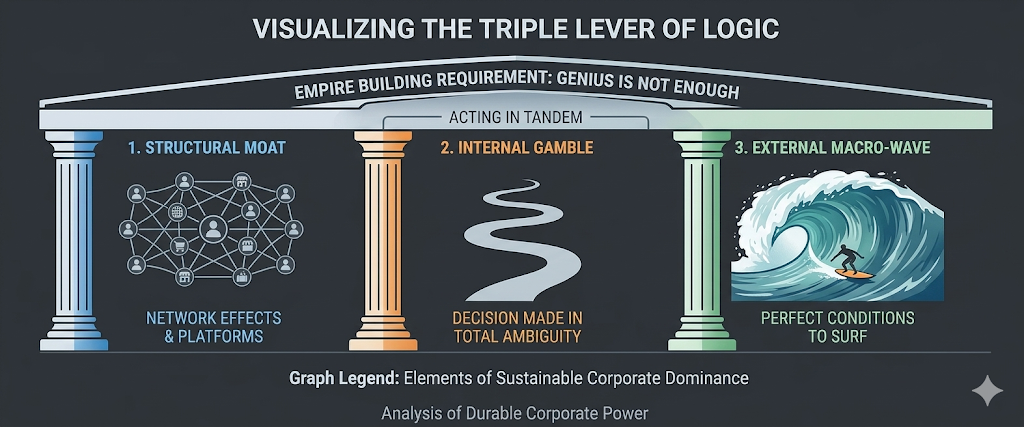

Because the world’s most powerful companies are powerful not primarily because of who founded them. They’re powerful because of specific strategic positions they occupied, specific moats they built, crucially, specific external conditions that amplified their advantages at precisely the right moment. Understanding that honestly doesn’t diminish what was built. It actually makes it more interesting.

What “Powerful” Actually Means in Corporate Terms

Before diving into the how, the what needs some precision.

“Most powerful” is not simply “largest.” Saudi Aramco, by revenue and resource control, is an entirely different kind of power from Apple. Saudi Aramco’s power is geopolitical and resource-based, it controls access to a commodity that the entire global economy runs on, and its ownership structure makes it an instrument of state as much as a commercial entity. Apple’s power is architectural, it operates a platform that has become infrastructure for hundreds of millions of people’s daily digital lives, creating switching costs and ecosystem lock-in that generate extraordinary, durable margins.

Microsoft’s power is partly legacy infrastructure, its enterprise software is embedded in the operational DNA of corporations and governments worldwide, and partly a now-genuine competition for the AI era’s foundational platform position. Amazon’s power is logistical and platform-based: it built the world’s most efficient retail distribution network, then used the cash flow from that network to fund AWS, which became the infrastructure underlying much of the global internet economy.

These are different types of power with different sources, different vulnerabilities, and different sustainability profiles.

Structural Patterns Behind Durable Corporate Power

Across the world’s most powerful companies, certain structural patterns appear consistently. They’re worth naming clearly.

Network effects are the most powerful and the most misunderstood. A network effect exists when a product or service becomes more valuable as more people use it. Visa and Mastercard benefit from this: a payment network is useful only if merchants accept it and cardholders carry it, creating a self-reinforcing loop. Meta’s social platforms operate on the same logic. Once a network effect is deeply established, the cost of displacing it is not just the cost of building a better product, it’s the cost of convincing millions of participants to move simultaneously, which is practically prohibitive.

Platform dominance is related but distinct. Platforms create marketplaces between producers and consumers. Amazon’s marketplace connects millions of sellers with hundreds of millions of buyers. Apple’s App Store connects developers with iPhone users. Google Search connects content producers with information seekers. Each platform extracts value from the marketplace it facilitates, through commissions, advertising, fees, while the two-sided network effects of the marketplace itself create the moat.

Proprietary technology with embedded switching costs is how enterprise software companies, SAP, Oracle, Salesforce, maintain pricing power despite offering products that are never the customer’s favorite. Once an enterprise has integrated its operational data into an ERP or CRM system, the cost of migrating in time, money, retraining, and operational risk is enormous. Companies pay premium prices for software they wouldn’t choose fresh partly because the exit cost is higher than the price increase.

Resource control explains different powers entirely. Saudi Aramco sits atop the world’s largest conventional oil reserves. Certain rare earth mining operations control materials that are essential inputs for electric vehicles, wind turbines, and advanced electronics. Resource power is geologically determined in ways that strategic brilliance cannot replicate which makes it simultaneously more durable and more politically exposed.

Also Read: Inside the Private World of Global CEOs and How the Most Powerful Executives Really Live

Moments That Actually Made the Difference

Behind every dominant company, there is typically not just a founding insight but a second strategic decision, often made under uncertainty, not with the clarity hindsight provides that created the moat.

Amazon’s decision to offer AWS as an external product, not just as internal infrastructure, was not obviously correct when it was made. It required believing that the capabilities Amazon had built for itself were generalizable enough to be a product, and that selling cloud infrastructure to potential competitors was strategically acceptable. It was a decision made in ambiguity that turned out to be the single most consequential strategic choice in the company’s history.

Microsoft’s decision, under Satya Nadella, to reorient away from Windows-centric thinking and toward cloud services was similarly non-obvious in its moment. Windows had defined Microsoft for three decades. Choosing to compete seriously in a cloud market where AWS had a commanding lead required accepting that the old source of power was diminishing and building a new one from a position of weakness. That kind of strategic self-disruption is rare in large organizations and harder than it sounds.

Apple’s decision to open the App Store to make the iPhone a platform rather than just a device transformed a hardware company into a platform company. It was a decision that created the conditions for the most valuable ecosystem in consumer technology history, and it required accepting that third-party developers would build significant value on Apple’s infrastructure, capturing it through a commission structure.

Each of these decisions looks obvious in retrospect. None was obvious when it was made.

What Actually Sustains Power Over Time

Building a dominant market position is one thing. Sustaining it across decades, through technological shifts, regulatory pressure, and competitive challenges, is different.

The companies that sustain power over time share a characteristic that is less discussed than their initial competitive advantages: they have governance structures that protect long-term decision-making from short-term market pressure. This takes different forms.

Some achieve it through dual-class share structures, Alphabet, Meta, and historically Amazon used structures that give founders and senior leadership disproportionate voting power relative to economic interest. This insulates strategy from activist shareholders demanding short-term returns.

Others achieve it through the sheer scale of their competitive moat. When a company’s market position is so strong that no realistic near-term competitor threatens it, management has structural freedom to invest in decade-long bets.

The companies that lose dominant positions almost always lose them through one of two mechanisms: either an external technological discontinuity that renders their core moat irrelevant (Kodak and digital photography; Nokia and smartphones), or internal organizational calcification, the inability to take on new strategic risks because existing success structures reward incremental improvement over transformational change.

The Regulatory Question Reshaping Corporate Power in 2026

The conversation about the world’s most powerful companies in 2026 cannot avoid the regulatory dimension. Antitrust action, data privacy regulation, platform liability frameworks, and AI governance requirements are all active policy areas that directly affect the structural position of the world’s largest corporations.

The European Union’s Digital Markets Act has created a new legal category the “gatekeeper,” for the largest digital platforms, imposing interoperability requirements, data-sharing obligations, and limits on self-preferencing that directly target the moat structures described above. In the United States, antitrust enforcement has become more aggressive after years of relative permissiveness, though the legal outcomes remain genuinely uncertain.

For the most powerful companies, regulation is not simply a compliance cost. It is a competitive dynamic. Regulatory requirements that are manageable for large established players can be prohibitive for smaller competitors. And the companies with the most sophisticated regulatory affairs operations, and the most invested relationships with regulatory bodies across multiple jurisdictions have a form of regulatory advantage that compounds over time.

Power in 2026 is partly the power to navigate the regulatory environment. The companies that understand that have built it into their strategic architecture.

Also Read: What Companies Actually Control the Global Economy

Final Verdict

The ultimate irony of corporate power is that it always feels permanent right up until the moment it isn’t.

When we look at the giants of 2026, it is easy to mistake their current ubiquity for immortality. We did the exact same thing with the railroad monopolies of the 19th century, the automotive titans of the 1950s, and the industrial conglomerates of the 1970s. The actors change, but the script remains remarkably consistent.

True corporate power is never a static achievement; it is a temporary lease on a specific historical moment.

The mythology of the brilliant founder in a garage is a comforting bedtime story we tell ourselves to make the vast, impersonal forces of global capitalism feel human-scaled. But the real story is far more interesting. Empires are built at the intersection of structural design, immense risk taken under the cover of darkness, and historical luck.

As we look toward the horizon,where artificial intelligence threatens to redraw the infrastructure of human thought and global regulators chip away at digital gatekeepers, the current titans will face the same ultimate test their predecessors did.

Those who survive will not do so because their founders were geniuses. They will survive if they can cannibalize their own success before an external shift does it for them. For the rest, the very moats they built to protect themselves will eventually become the trenches in which they are trapped.

FAQs – Frequently Asked Questions

True corporate power involves durable structural advantages, network effects, platform position, proprietary technology, resource control, or regulatory positioning that protect margins and market position over time, not just current size or revenue.

History suggests yes, but usually through technological discontinuity that renders existing moats irrelevant, not through direct head-to-head competition in the core market. The smartphone era disrupted PC-era dominance; the AI era may similarly reshape current platform hierarchies.

Dual-class or founder-controlled share structures exist to insulate long-term strategic decision-making from short-term shareholder pressure, allowing the kind of decade-long platform bets that created dominant market positions in the first place.

Regulation reshapes competitive moats, sometimes by attacking them directly, sometimes by creating compliance requirements that large players absorb more efficiently than smaller competitors. The net regulatory effect is more complex than it appears.

Technological discontinuity remains the most consistent historical threat. Companies whose core moats are built on specific technology paradigms are vulnerable if a new paradigm renders those assets less central.

AI answers user queries directly instead of driving traffic to external apps or web links. This bypasses and collapses traditional revenue engines like search ads and app store commissions.

Modern giants freeze out competition by weaving hardware, data, and identity into a single web. Leaving causes so much daily friction that users stay trapped even without high prices.

Yes, because platforms like AWS or Azure operate as core public utilities. Breaking them up

risks destabilizing the critical cloud infrastructure that keeps global commerce and governments running.

Dwayne Paschke is a seasoned content strategist and AI automation specialist with over nine years of experience at the intersection of journalism and digital innovation. A versatile force in the media landscape, Dwayne has built a reputation as an expert content writer and investigative journalist, contributing high-impact pieces to various reputable news websites.